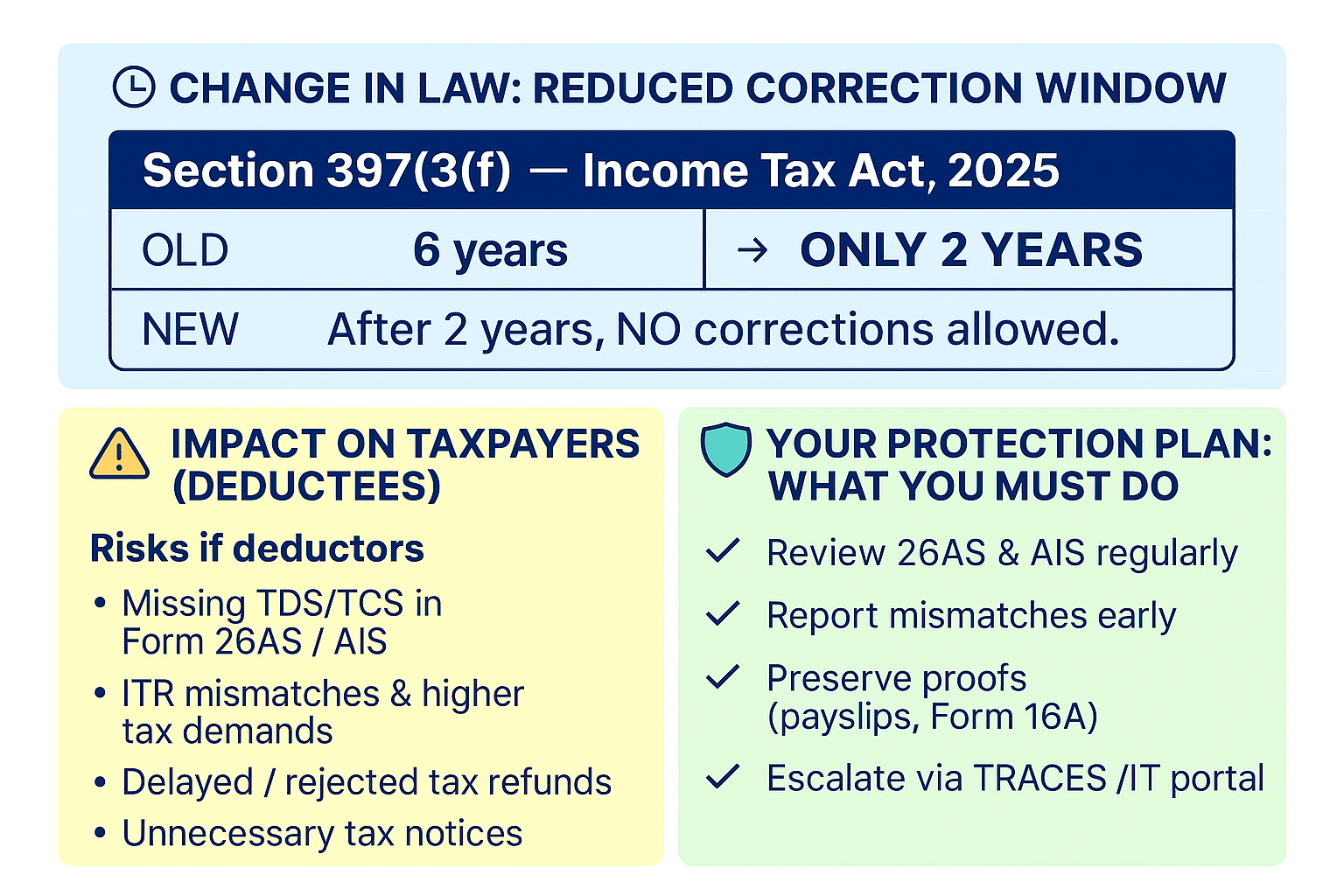

Time Limit to revise TDS Return – Change in Section 397(3)(f) of the Income Tax Act, 2025

TDS Return revision time limit has been changed to 2 years from 6 years after amendment in section 397(3)(f) of Income Tax Act, 2025

TDS Return revision time limit has been changed to 2 years from 6 years after amendment in section 397(3)(f) of Income Tax Act, 2025

Companies follow different methods of TDS accounting – Accrual based v/s Receipt based accounting. With an objective to reconcile sales and TDS both with 26as form, which method is more suited?

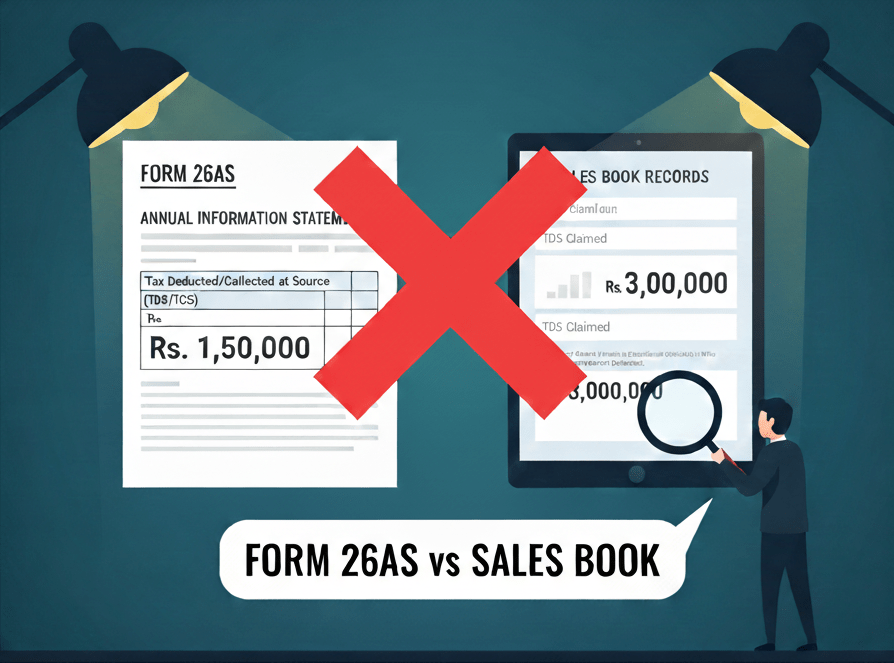

Explore possible reasons for Tax Credit mismatch with Form 26as, how to resolve them and best practices for 26as reconciliation with books

In order to simplify direct tax in India, Government has omiyyed section 206AB, 206CCA, 206C(1H) from Income Tax Act 1961.

TaxReco’s Data Transformation Module can automate data cleaning and transformation activity, which is essential before TDS Payable reconciliation

Issues faced in 26AS Reconciliation and their possible solutions using tax technology like TAN to PAN search

The concept of TDS was introduced with an aim to collect tax from the very source of income. As per this concept, a person/company (deductor) who is liable to make payment of specified nature to any other person/company (deductee) shall deduct tax at source and remit the same into the account of the Central Government

Technology has made inroads into every function of business. How can tax function stay away from this?

While we are automating TDS Reconciliation (26AS Reconciliation & 34A Reconciliation) for customers – we would like to share recent experiences and instead redefine the purpose of automation.

Bringing technology into business for core administration tasks has been cited as one of the innovations that has rescued most corporate tax departments over the last two years…